Credit for the next phase of the business cycle

Financial markets are at an interesting juncture.

Global equities have been in a broad trading range over the past 15 months, interspersed by two episodes of considerable volatility, first in the summer of 2015, and then again in early 2016. Similarly, global bond yields have fluctuated in a wide band, reflecting sizeable shifts in the outlook for economic growth and inflation. For all the capital market movements, no sustainable trend has materialized, leaving investors wondering what will come next.

Tug of war points to credit's relative attractiveness

The tug of war in asset prices represents a complex mix of economic, financial, and political drivers: On one side are weak growth statistics and corporate cash flows, expensive valuations for many financial assets, and a rising political risk premium across the globe. On the other side are innovative central bank stimulus measures designed to support the broader economy in general and financial markets in particular. Taking all of this into consideration, we prefer assets higher in the capital structure, and the current House View at Standard Life Investments reflects a heavy emphasis on investment-grade corporate credit.

Following the most recent bout of market volatility, corporate credit is attractively valued relative to government debt, which offers much lower yields. Credit also remains an effective way to hedge exposure to equity, which is more vulnerable to sharp price fluctuations. Furthermore, the hunger for investment income—roughly a quarter of the global government bond market now generates a negative yield—and the possibility of further European Central Bank (ECB) purchases of corporate bonds also supports this favorable view of credit.

A focused approach toward other risk assets

We believe that monetary authorities will take sufficient action to forestall any material slowdown in the global economy. However, we also believe that these policymakers will resist the siren calls from some quarters for helicopter money—which refers to irrevocable stimulus measures taking any number of forms, including tax rebates—that could lead to a major change in inflation expectations. Although central banks in many regions are calling for more supportive fiscal policy and structural reforms to drive activity, most governments, in our view, are not yet in a position to agree. Accordingly, the portfolios we manage for clients are still positioned for a medium-term outlook of moderate but positive corporate cash flows, supporting a focused approach toward risk assets.

Current investment opportunities aren't limited to the credit markets. Our view is also positive on global real estate assetsin general and those with exposure to continental Europe commercial property in particular. More expensive areas, such as parts of the U.K.'s real estate market, face a supply and demand balance less favorable to prospective investors.

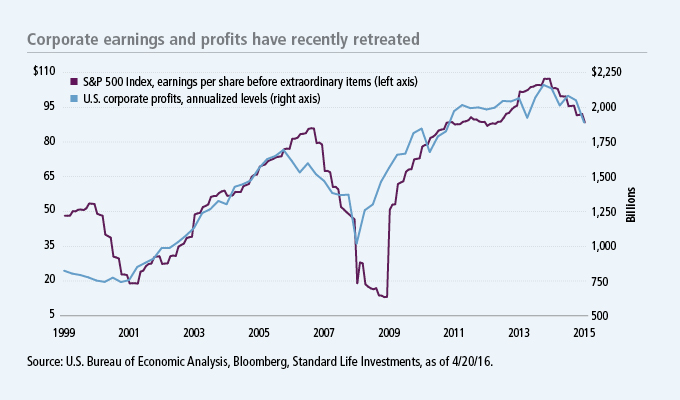

We also expect stocks to perform moderately well in this low growth environment, although not without moments of high price volatility, which may provide rebalancing opportunities. The good news for equities is that surveys of fund manager positions reveal relatively high cash levels, reflecting a cautious sentiment overall. The bad news is that stock market valuations are not offering much room for error. In the United States, corporate earnings are coming under pressure from the weakness in top-line sales growth, and the consensus does not expect an immediate recovery in profit growth.

Prospects in Europe look better. On the whole, we favor European assets over their counterparts in other parts of the world. European equities may benefit from improving corporate competitiveness, a rise in domestic demand, and disciplined cost-cutting measures. Meanwhile, regulatory-driven demand and the ECB's bond-buying programs support European debt. Regardless of geographical region, right now we favor assets higher in the corporate capital structure, and investment-grade credit offers a comparatively compelling risk/reward profile in a macroeconomic environment marked by uncertainty.